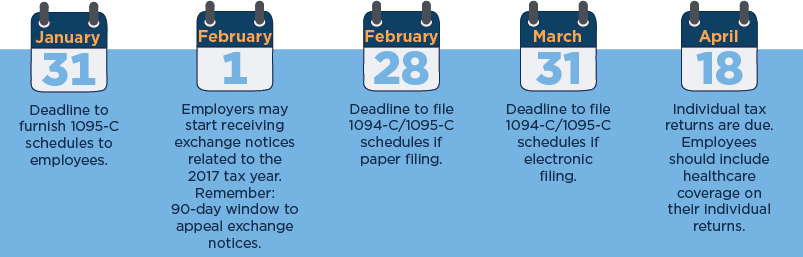

Avoid These 4 Common ACA Reporting Mistakes

1. Applicable Large Employer “ALE” Member Identification & Responsibilities

- Failure to understand the IRS penalties for not complying with the ACA including,

- the employers shared responsibility payment for failure to offer minimum essential coverage,

- employers shared responsibility payment for failure to offer affordable minimum essential coverage that provides minimum value (assessed if penalty 1 does not apply),

- failure to file correct information returns, and,

- failure to furnish correct payee statements.

- Failure to perform annual ACA testing.

- Failure to accurately combine ALE employer and employee information.

- Failure to include any other ALE members on the 1094-C Part IV report.

2. Measurement, Stability, and Employment Periods

- Failure to establish annual measurement and stability periods for determining which employees are to be offered health care coverage by the employer.

- Failure to document all information necessary to identify full-time employees.

- Failure to adopt policies explaining,

- its look back measurement period,

- description of how the employer is classifying its new employees, and,

- explanation of the time frames and start/end dates of the non-compliant measurement, Administrative, or Stability Period.

- Erroneous reporting of employment periods including hire, rehire, and termination dates in Payroll and Time & Attendance platforms. (e.g. Inaccurate documentation explaining how an employee who has been rehired is a new or continuing employee.)

- Failure to oversee disruptions in service of 13 weeks (or 26 weeks for an employee of an academic organization) for purposes of reconciling with employment status and with health benefits eligibility.

3. Classifying Employees

- Failure to organize and accurately document employment classification with one of four labels:

- Full-Time

- Part-Time

- Variable Hour

- Seasonal

- Misclassification of an employee, leading to the risk of a penalty. (e.g. Classifying new employees, who should be classified as full-time employees, as part-time employees or variable hour employees.)

- Misclassification of contingent workers, leading to the risk of a penalty. (e.g. Freelancers, independent contractors, consultants, or other outsourced and non-permanent workers who are hired on a per-project basis are misclassified as full-time employees.)

4. Health Benefits

- Failure to explain which affordability safe harbor the employer has elected to use.

- Failure to document affordability plan for the employee.

- Failure to sufficiently document offers of health coverage, including an explanation of the product being offered, effective applicability dates, the price of each option, and whether the coverage provides minimum value.

- Failure to document when the health coverage offer was made. (e.g. Employee not returning his/her selection of coverage or waiver.)

- Lack of awareness of the effect of Flex Credits (amount employer gives employees to purchase benefits), opt-out payments (payments made to employees who decline enrollment in an employer’s group health plan), and similar arrangements on the reportable amount of the employee’s required contribution to the monthly premium on line 15 of the 1095-C.

- Errors in reporting on the Form 1094-C and Form 1095-C. (e.g. Inaccurate code combinations on line 14, 15, and 16 of Form 1095-C.)

To receive insights and a free risk assessment of your company’s ACA compliance practices with our HR industry experts call us at (844) 398-7800, or email us at getstarted@highflyerhr.com.